I. Introduction: The Category Error of Modern Finance

Mainstream economic thought treats inflation as a phenomenon of monetary volume—the "Too Much Money" paradigm. However, by applying the engineering logic of C.H. Douglas’s A+B Theorem, we can deduce that inflation is not primarily a result of consumer behaviour, but a mathematical consequence of debt-based cost accounting in an industrial society.

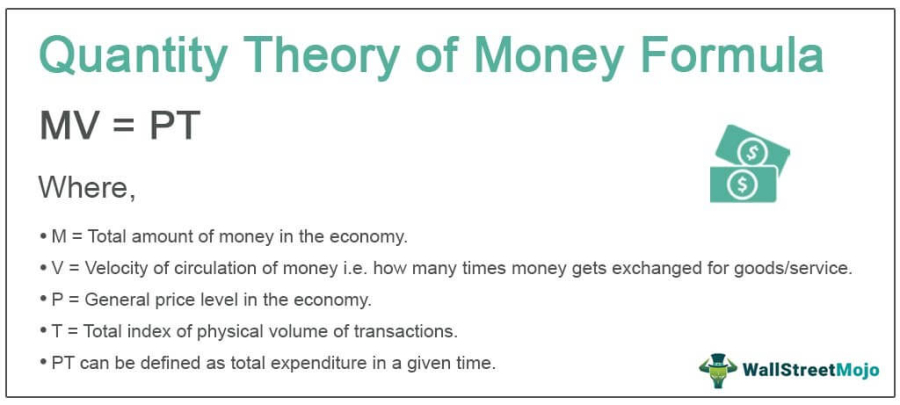

II. The Quantity Theory of Money (QTM): The Marketplace View

The orthodox explanation for inflation is the Quantity Theory of Money, mathematically expressed through the Equation of Exchange:

MV = PY

Where M is the money supply, V is the velocity (how often money changes hands), P is the price level, and Y is the total output.

The QTM View of Inflation

The QTM assumes that V and Y are relatively stable. Therefore, any increase in the money supply (M) must lead to a proportional increase in prices (P).

- The "Too Much Money" Logic: Inflation is seen as "demand-pull." If the government or banks "print" too many tokens, consumers bid up the prices of a limited supply of goods.

- The Solution: To stop inflation, the central bank must restrict the money supply or raise interest rates to "cool" spending.

III. Why Douglas Rejects the QTM: The Linear Flow of Credit

Douglas rejects the QTM because it relies on a "flea market" fallacy—the assumption that money is a fixed commodity that circulates indefinitely. In a modern industrial economy, Douglas observes that money is a temporary credit entry.

- Creation: Money is created by banks as a debt-entry to fund production.

- Destruction: Money is destroyed and cancelled the moment it is repaid to the bank.

The Logical Rebuttal: Because money is destroyed upon repayment, it cannot "circulate" forever. If a dollar is used to pay for a machine cost (a B-payment), it is cancelled out of existence by the bank. It is no longer available to buy the goods the machine produces. The QTM fails because it ignores this rate of destruction, assuming a stagnant "pool" where there is actually only a "flow" constantly evaporated by debt-repayment.

IV. The A+B Theorem: The Flow of Costs vs. Income

Douglas’s theorem replaces "pool" logic with "flow" logic, dividing payments into:

- Group A: Payments to individuals (wages, salaries, dividends).

- Group B: Payments to other organizations (raw materials, bank charges, machinery).

The total price of a product is A + B. However, since only A represents current purchasing power, and the money for B is often cancelled via debt-repayment before the goods hit the shelf, there is a structural gap where A < A + B.

V. The Technological Proof: The Divergence of A and B

As technology (T) advances, the ratio between Group A and Group B shifts permanently because innovation replaces human effort (A) with mechanical efficiency (B).

Example: The Road-Building Evolution

- Pre-Industrial: 100 men with shovels. Most costs are wages (A).

- Industrial: 1 man with a $500,000 excavator. Wages (A) plummet, but the costs of debt, maintenance, and depreciation (B) skyrocket.

The Proof of the Gap: If Total Price = A + B, and technology ensures B costs increase as a percentage of total costs, the purchasing power of the public is constantly diminishing. As technology advances, B payments increase relative to A payments.

VI. The Stabilization Trap: Mathematical Proof of Inflation

The "Stabilization Trap" occurs when the state attempts to keep $A$ (income) constant to maintain "Full Employment" while machines are replacing workers.

Mathematical Proof:

- Let the Price Pool be P = A + B.

- Define the ratio of overhead to labor as k = B/A. Thus, P = A*(1 + k).

- As technology advances, k increases dk/dt > 0.

- To keep A stable, the system must initiate New Production financed by New Debt (D).

- While this D provides immediate wages A{new}, it carries its own future overhead B{new}.

- Because k is always rising, the amount of total price (P) generated to create a single unit of A grows exponentially:

P{total} = A{stable} * (1 + k{rising})

Conclusion: Any attempt to maintain wages through new debt-driven work leads to a disproportionate explosion in future costs. This Cost-Push Inflation is more consistent with Credit Money (created and destroyed) than with the belief that money circulates. We are effectively "printing" future prices to pay for current survival.

VII. The Phillips Curve: A Structural Trap

The Phillips Curve traditionally illustrates an inverse relationship between unemployment and inflation. The A+B Theorem identifies this as a structural liquidity trap inherent to debt-based accounting.

Solving the Trade-off

The A+B Theorem explains the trade-off more accurately than the QTM:

- The "Inflation" Choice (Full Employment): To lower unemployment, the system injects new "A" payments via new production (A+B). Since B is disproportionately large in a technological age, creating enough "A" to sustain the public floods the market with a much larger volume of future "B" costs. Inflation is the result.

- The "Unemployment" Choice (Deflation): To stop inflation, the state restricts credit. This stops "B" costs from rising but starves the system of "A" payments. In an A+B deficit, the public cannot pay for existing production, leading to bankruptcies and unemployment.

Explaining Stagflation

The A+B Theorem explains Stagflation (simultaneous high inflation and unemployment). "B" costs from previous debt-heavy cycles hit the market as high prices, while the restriction of new credit cuts off current "A" payments (wages). Unlike the QTM, Douglas shows prices must remain high to satisfy past debt-accounting, even if demand is non-existent.

VIII. Final Comparison

|

Feature |

Quantity Theory (QTM) |

A+B Theorem (Douglas) |

|

Logic |

Marketplace (Tokens) |

Factory (Accounting) |

|

Money Lifecycle |

Eternal Circulation |

Creation & Destruction |

|

Primary Driver |

Volume of Money (M) |

Accumulation of B-costs |

|

Stagflation |

Anomalous/Unexplained |

Logical Accounting Result |

IX. Conclusion

The Quantity Theory is a pre-industrial observation. The A+B Theorem demonstrates that inflation is the "exhaust" of a debt-based engine. To fix inflation without creating unemployment, the system must stop filling the gap with debt and start filling it with debt-free credit via the Compensated Price Mechanism. By issuing credit directly to retailers to discount prices at the point of sale, the system can mathematically cancel the "B" costs, allowing the public to purchase the total production with their existing "A" income without triggering a price-wage spiral.