The rapid growth of Canada's federal debt from the mid-1970s onwards is one of the most contentious topics in Canadian economic history. One common narrative, often amplified in alternative economic circles, points to a pivotal 1974 policy shift under Prime Minister Pierre Trudeau — involving greater alignment with the Bank for International Settlements (BIS) and its Basel Committee recommendations — as the moment when Canada abandoned low-cost financing through the Bank of Canada in favour of borrowing from private financial markets at compound interest. The critics argue that this was what triggered the subsequent exponential growth in federal debt levels. Central to this framing of the facts is a citation from the Auditor General of Canada's 1993 report, which appears to show that compound interest, rather than programme spending, drove the vast majority of accumulated debt.

In what follows, I wish to address this claim in some detail. I will first present the Auditor General's findings, analyze the strengths and limitations of the dominant framing, offer an alternative causal perspective grounded in fiscal flows and policy agency, demonstrate why the alternative explanation is more accurate, and finally explore how the 1974 shift functioned — within the constraints of the conventional monetary system — as a palliative mechanism for injecting purchasing power to address structural demand gaps, albeit at significant long-term cost. This analysis draws on standard public finance principles while incorporating the vitally important insights of C.H. Douglas’ Social Credit financial and economic analysis.

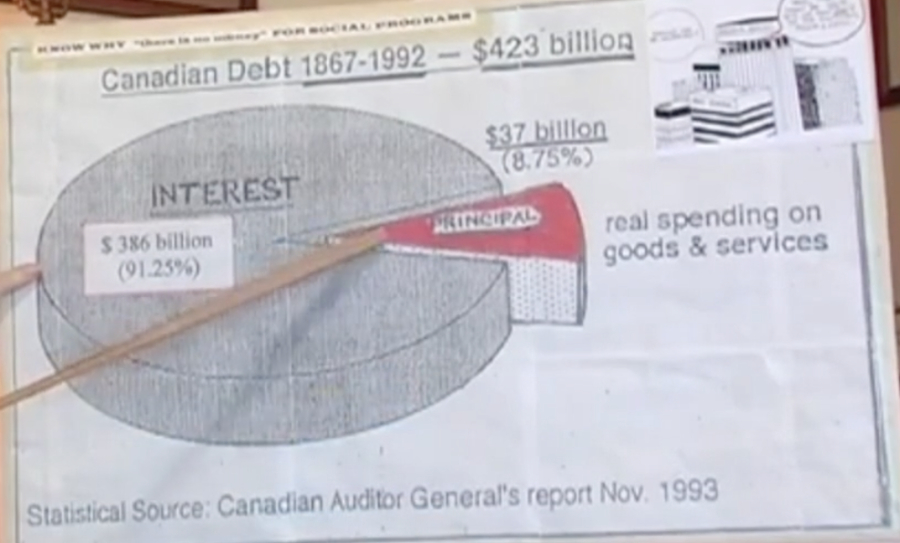

- a) The Auditor General's Claims (1993 Report)

In its 1993 report to the House of Commons, the Office of the Auditor General of Canada provided a striking long-term decomposition of federal debt accumulation. Covering the period from Confederation in 1867 through to the fiscal year 1991-92, the report (notably in Section 5.41) observed that the federal government's net debt had reached approximately $423 billion.[1]

Of this total, only about $37 billion represented the cumulative net shortfall in meeting the costs of government programmes (goods, services, transfers, and other non-interest expenditures) over the entire 125-year history. The remaining $386 billion — roughly 91% of the accumulated debt — was attributed to the cost of borrowing and the compounding effects of interest payments on earlier debt. In 1991-92 alone, interest on the debt amounted to $41 billion, a major contributor to that year's deficit

The report framed interest not merely as one annual expense, but as a powerful amplifying force: once primary shortfalls created initial debt, interest obligations grew exponentially unless offset by surpluses, economic growth, or inflation. This retrospective accounting exercise highlighted how relatively modest cumulative programme shortfalls, left unaddressed over decades, had ballooned into a massive debt stock due to compounding interest.

Proponents of this "debt trap" narrative often pair the data with pre- and post-1974 debt figures. From 1938 to 1974, it is claimed that the Bank of Canada acted more like a public utility, providing low- or near-interest-free loans for major infrastructure (e.g., the Trans-Canada Highway, St. Lawrence Seaway). Federal debt remained relatively stable, rising modestly to around $20-21 billion by 1974. After the shift toward private market borrowing, debt surged to roughly $160 billion by the end of Pierre Trudeau's tenure in 1984 and continued climbing sharply thereafter.

This data has been widely cited to argue that the 1974 pivot — ending preferential central bank financing in favour of market-rate borrowing aligned with international norms — marked the beginning of an unsustainable exponential growth in debt driven by private compound interest.

- b) The Dominant Framing and Its Limitations

The standard interpretation of the Auditor General's numbers is a retrospective stock decomposition. It treats the $423 billion net debt as a final accumulated pile and asks: how much of this ending balance originated from "real" programme spending shortfalls versus interest compounding on prior borrowing? The answer — only was 8-9% primary, 91%+ was interest — leads to the claim that "interest caused most of the debt."

This framing has rhetorical power. It vividly illustrates the self-reinforcing nature of debt: past deficits create interest costs that require further borrowing, which generates more interest, and so on. It supports critiques of the post-1974 system as eroding monetary sovereignty and turning government into a vehicle for transferring taxpayer funds to private bondholders. In this view, the government shifted from "builder" (using cheap public credit for productive infrastructure) to "debtor" trapped in a cycle dictated by international markets and the BIS.

But what is wrong with this framing? Several issues arise when this interpretation of the raw data is presented as if compound interest were the primary causal explanation:

- It confuses accounting attribution with forward-looking causality. The decomposition is a valid counterfactual exercise: If there had been no interest costs and the same programme spending levels, the total outstanding debt would have been far smaller (closer to the $37 billion cumulative primary shortfall). But this does not mean interest was an independent, exogenous force that "caused" the borrowing. The interest was rather a consequence of prior borrowing, which itself stemmed from policy decisions.

- It obscures the flow mechanics of government budgeting. In reality, interest is a prioritized annual expenditure paid primarily from current tax revenues. New borrowing finances the overall deficit: total spending (programmes + interest) minus total revenue. Borrowing is not typically "used to pay interest" in a direct sense; rather, it enables governments to sustain desired programme levels when revenue after interest falls short. The entire debt stock thus reflects cumulative choices to spend beyond revenue.

- It downplays agency and policy choices. Governments were not mechanically forced into ever-larger deficits solely by interest. They could have restrained programme growth, raised taxes, or run primary surpluses (non-interest revenue exceeding non-interest spending) to stabilize the debt trajectory. The fact that they often chose not to — amid economic challenges like stagflation, recessions, and political priorities — is central to understanding the rate of growth. The successful 1990s turnaround under Prime Ministers Chrétien and Martin, which involved significant programme restraint, demonstrated that choices mattered.

- It risks rhetorical sleight-of-hand. Saying "91% of the debt is interest, not real spending" can misleadingly imply that programme spending was minimal or irrelevant, when in fact vast sums were spent on various programmes over decades. The debt records the borrowed portion of that spending, enabled by decisions to run overall deficits rather than live within (post-interest) means.

In sum, while the framing is useful for highlighting the role of compound interest, it becomes misleading when it is used to obscure fiscal policy, i.e., when it is used to portray the debt as almost entirely a product of a 1974 "pivot" rather than sustained overspending relative to revenue.

- c) An Alternative Framing: Causal Flow, Payment Priority, and Policy Agency

A more accurate perspective, in my view, would be to consider the entire $423 billion (and subsequent growth) through the lens of annual fiscal flows and policy choices. Debt accumulates because, year after year, governments decide to spend more than they collect in revenue. Interest is a real and growing component of spending — a mandatory priority claim on tax revenue — but it does not autonomously drive new borrowing. New debt arises when total desired expenditures (programmes plus interest) exceed revenue.

In this view:

- Tax revenue first services interest and other obligations.

- Remaining revenue supports programmes.

- If governments wish to maintain or expand programmes beyond what is left, they borrow the difference. That borrowing supports higher programme activity than a balanced budget would allow.

- Over time, the full debt stock represents the cumulative record of programme spending financed by borrowing due to insufficient revenue after interest.

The Auditor General's $37 billion figure usefully shows the net primary shortfall after all compounding. But it does not mean only $37 billion in borrowings was "spent on programmes." Far more was spent; the debt simply captures the excess over sustainable tax financing. The higher interest burden post-1974 reduced fiscal space, requiring larger deficits to sustain programme levels — but this was a policy choice, not an inevitability.

- d) Why the Alternative Framing Is Superior

The causal flow/policy agency perspective is more accurate for several reasons:

- Better causality: It correctly identifies repeated decisions to run overall deficits as the fundamental cause behind the growing debt. The stock decomposition is backward-looking arithmetic; the flow view explains why the pile kept growing year after year.

- Aligns with accounting reality: Governments budget and borrow on a flow basis. Interest is paid from current revenues; borrowing fills the total gap.

- Emphasizes accountability: It holds elected governments responsible for spending and revenue choices rather than attributing outcomes primarily to "the system," compound interest, or the BIS. This is crucial for understanding both the problem and putative solutions (e.g., the 1990s restraint that stabilized the growth in debt).

- Avoids misleading implications: It acknowledges that without interest costs, debt would have been lower for the same programmes, but does not suggest that programme spending was insignificant.

- Compatibility with heterodox insights: It accommodates demand-side concerns without romanticizing debt.

The Auditor General numbers remain valuable as a warning about compounding, but are better interpreted through this lens than as proof that interest "caused" the debt independently.

- e) The 1974 Shift as a Palliative for Demand Injection in the Conventional System

Within the context of Social Credit theory, C.H. Douglas identified a structural "price-income gap" defined by the A+B theorem: the costs/prices generated in production (including bank charges, depreciation, etc.) exceed the incomes simultaneously distributed to consumers. This can lead to an insufficiency in consumer purchasing power, gluts, and economic instability unless addressed.

In the conventional debt-based monetary system, one blunt way to bridge this gap is government deficit spending: borrowing money to inject additional purchasing power through programmes, transfers, and related expenditures. Interest payments further recycle funds to bondholders, who spend or invest portions of it.

The post-1974 shift to market-rate private borrowing had the effect — whether intended or not — of facilitating greater net injection under this system, at least for a time:

- Higher interest costs claimed a larger share of tax revenue, shrinking the fiscal space available for programmes from taxes alone.

- To sustain or expand desired programme levels (and thus economic support), governments ran larger overall deficits, issuing more debt.

- This new borrowing directly funded additional programme spending, injecting money into the economy.

- Simultaneously, interest payments redistributed tax revenue to bondholders (banks, pension funds, individuals), some of which flowed back as consumption or investment.

In this sense, the higher interest burden acted as an automatic (if inefficient) mechanism that "created space" for greater deficit-financed injection. It allowed the conventional system to pump more purchasing power into circulation to address any price-income gap, supporting demand amid stagflation and structural changes. This was palliative: it provided short-to-medium-term relief without fundamental reform, enabling continued programme expansion beyond immediate tax capacity.

However, as acknowledged, this came with heavy long-term costs: compounding debt servicing obligations, reduced fiscal flexibility, higher future taxes or cuts, potential crowding out of private investment, and eventual austerity. Social Credit alternatives — such as a National Dividend (direct consumer credits distributed periodically to citizens) and compensated price discounts — would have been a superior approach, injecting additional purchasing power without accumulating interest-bearing debt or relying on ever-growing deficits. The 1974 shift did not solve the gap; it managed it in a costly, unsustainable way within the existing framework.

Conclusion

The Auditor General's 1993 decomposition powerfully illustrates the dangers of compound interest, but should not be read as evidence that interest alone caused Canada's debt crisis. A causal flow perspective centered on policy choices to spend beyond revenue, with interest as a prioritized constraint and amplifier, more accurately reflects the actual reality. The 1974 shift amplified these dynamics, functioning as a flawed palliative that enabled greater monetary injection to support demand — consistent with the Social Credit diagnosis concerning the chronic, underlying gap in consumer purchasing power — while sowing seeds for later instability.

Understanding this question concerning federal debt in precise terms matters. It moves us beyond simplistic "debt trap" stories or denials of fiscal pressures toward a nuanced recognition of trade-offs, agency, and alternatives. Sustainable fiscal policy requires primary balance discipline, growth-enhancing reforms, and — in line with the Douglas Social Credit monetary reform proposals — exploration of more direct, less burdensome mechanisms to ensure adequate purchasing power. Canada's experience from 1974 onward offers lessons in both the power and perils of relying on debt-financed demand management.

[1] https://publications.gc.ca/collections/collection_2015/bvg-oag/FA1-1-1993-eng.pdf